Why a TFSA May Be Your Most Important Investment Account - Case Study

Your TFSA is one of the most powerful tools in your financial arsenal. Use it right!

FINANCIAL PLANNINGTAX PLANNINGRETIREMENT PLANNING

Steven

7/15/20256 min read

If you asked a financial expert "What's the best type of investment account to open?" you could probably expect the answer "Well, it depends"....and while that's technically the correct answer, there is a very strong case for why many investors are getting it wrong by not maximizing their TFSA (Tax-Free Savings Account). Let's get into it.

What's a TFSA?

A TFSA (Tax-Free Savings Account) is a type of savings account in Canada that lets you:

Grow your money tax-free (no tax on interest, dividends, or capital gains)

Withdraw money anytime without paying tax

You can use it for saving or investing, and it won’t affect your income taxes when you take the money out.

The only big rule that is imposed by the Canada Revenue Agency on this account type is an annual contribution limit. But if you don't use it, it will carry forward to the next year and stack with other un-used contribution room.

What's the problem?

Many investors fail to maximize the true power of their TFSA because they don't understand the importance of the account. Perhaps they don't contribute to it each year or use it as short term savings account with their bank. In either case, understanding the mechanics of the TFSA and how it fits within a broader financial plan is important for every Canadian.

It's often argued that a TFSA is best for lower income earners, but an RRSP is more effective for higher income earners because of the tax deductions that come through RRSP contributions. Again, while that's technically true, it may not be the best strategy when considered in the context of your financial plan.

Case Study

To analyze this, let's take a look a look at the financial plans for 3 individuals to see how maximizing their TFSAs first is usually in their best interest. All three of them live in Ontario, are 25 years old now, plan to retire at 65 and will save approximately 18% of their income or the RRSP maximum in a 60/40 balanced portfolio towards retirement. The only differences are their annual incomes, current expenses and spending goals in retirement. Let's introduce them.

Janice, a physician making $250,000/year, with expenses of $137,000 and a spending goal of $90,000 during retirement.

Paul, a sales manager making $150,000/year, with expenses of $85,000 and a spending goal of $70,000 during retirement.

Clayton, a handyman making $50,000/year, with expenses of $35,000 and a spending goal of $40,000 during retirement.

Using advanced financial planning software, we're going to evaluate the decision to max out their RRSP each year or deposit into their TFSA first, and then max out their RRSP with the remainder.

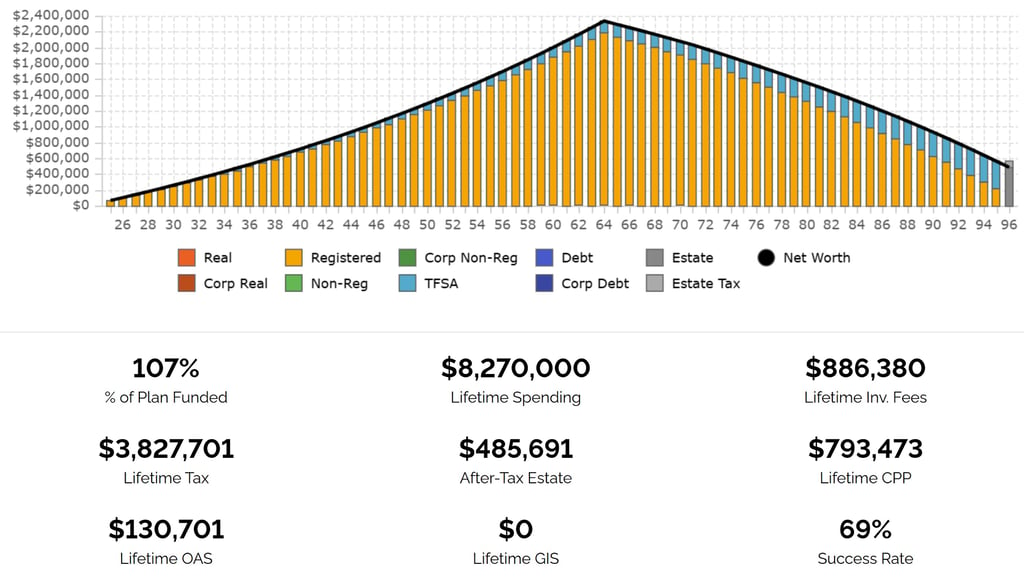

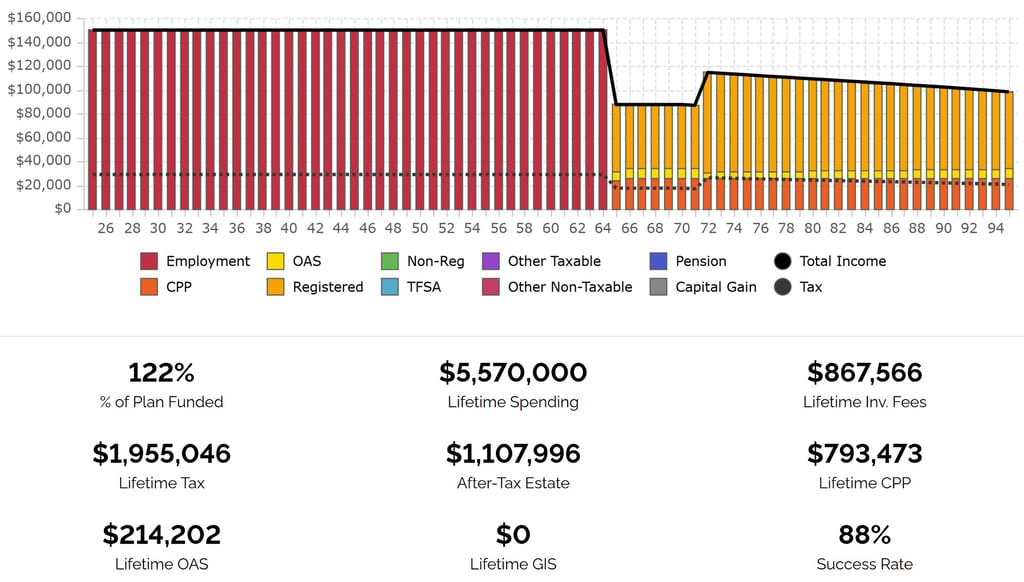

Case #1 - Janice

Janice benefits the most from her RRSP contributions as she's in a 49.85% marginal tax bracket and the RRSP deductions generate significant tax savings. She's even able to direct additional funds into her TFSA. When she retires her RRSP is worth $2.1M and her TFSA worth $150K. Overall, the success rate of 69% on her retirement plan confirms that she does have some flexibility to absorb poor market performance, but the plan isn't without risk. When she passes away at age 95, she'll be able to pass on up to $485K to her beneficiaries after a $75K tax bill.

Janice Net Worth Chart for RRSP First Scenario

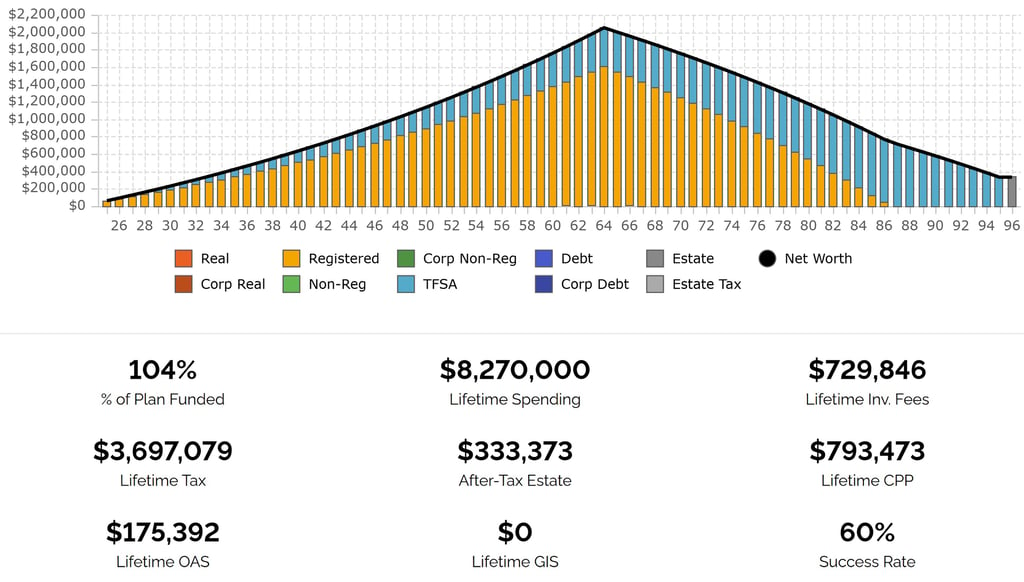

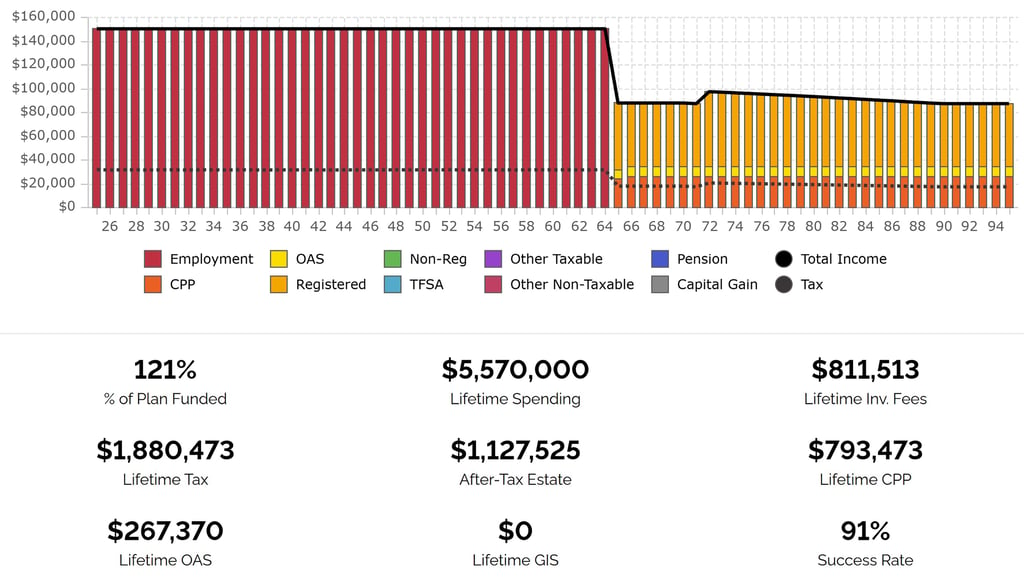

Now let's see what happens when she instead maxes out her TFSA first, and then contributes the rest into her RRSP. Because she's not receiving as many tax deductions she misses out on the opportunity to save more in her RRSP once the TFSA contribution has been made. The success rate of her plan decreases to 60% largely because she simply has less savings to draw from during retirement. She will receive more Old Age Security (OAS) and pay less in taxes over the life of her plan with this approach, but many of those benefits don't appear until later in retirement. At face value, the RRSP-first scenario may be a better choice for Janice. But, there are a few reasons why her TFSA may still be her most important account.

Janice Net Worth Chart for TFSA First Scenario

Net Worth Chart for TFSA First Scenario

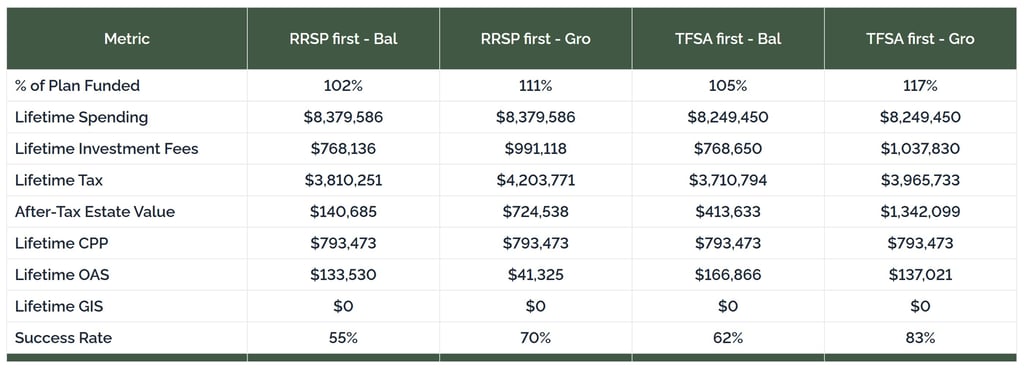

Let's consider what happens if Janice met with a financial planner who took the time to go through a risk profile with her and explained the history of investment returns. After the discussion, she decided to switch her portfolio to a "growth" asset allocation given her long investment time horizon and ability to meet current expenses comfortably. With this single change to her plan, the difference between the RRSP first or TFSA first strategy is only 1% in terms of success rate. But she'll have more flexibility during retirement and her after-tax estate will actually be larger at age 95 by using the TFSA first. A full comparison of all 4 scenarios is below:

Comparison Table for Janice Balanced or Growth Investor Scenarios

Case #2 - Paul

Similar to Janice, Paul's RRSP contributions during his working years allow him to save on taxes and accumulate more in savings. Even though his net worth leading into retirement would be higher in the RRSP first scenario, the succuss rate of his plan is actually lower with this approach. The benefits of the TFSA first strategy are perhaps most pronounced when we compare his projected income sources throughout retirement with the charts below. With the RRSP first strategy, the annual minimum RRIF withdrawals starting at age 72 push him above the OAS claw-back threshold and into a higher tax bracket.

Paul Annual Income Sources for RRSP First Scenario

Conversely, in the TFSA first scenario, we notice right away that his RRSP minimum withdrawals starting at age 72 don't cause the same jump in taxable income. This results in less of his OAS being clawed back and decreases his tax rate. With a 91% success rate on the plan, Paul could likely afford to increase his retirement spending goal if his portfolio has higher returns early in retirement.

Paul Annual Income Sources for TFSA First Scenario

Case #3 - Clayton

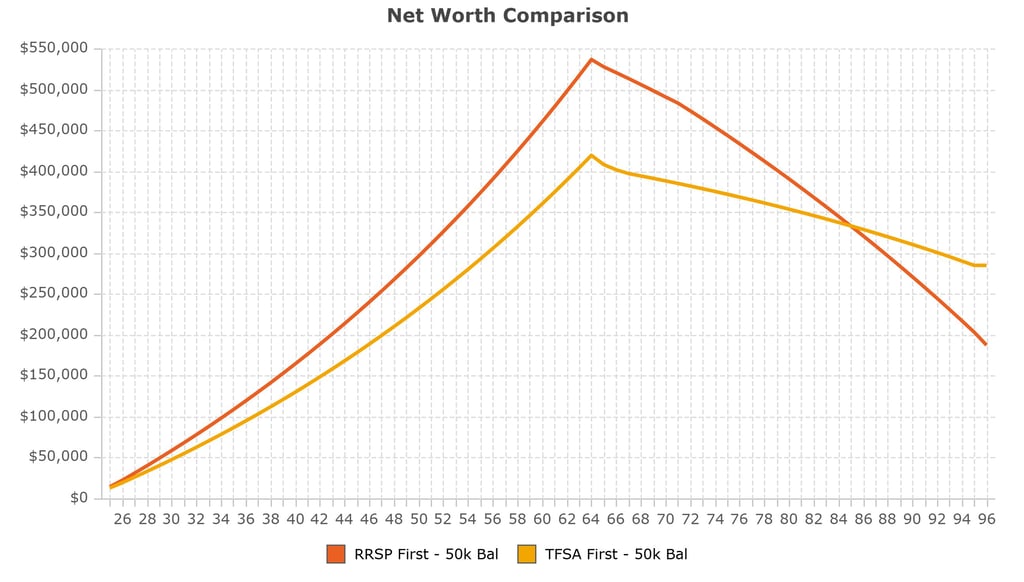

As a lower income earner, the benefits from Clayton's RRSP contributions are not as stark as they would be for Janice & Paul, but they shouldn't be ignored. If he maxes out his RRSP each year his net worth will grow faster than it would with a TFSA contribution. But he's sacrificing benefits now for stability in the future. The chart below shows how his net worth would change between the two scenarios.

Clayton Net Worth Comparison Chart

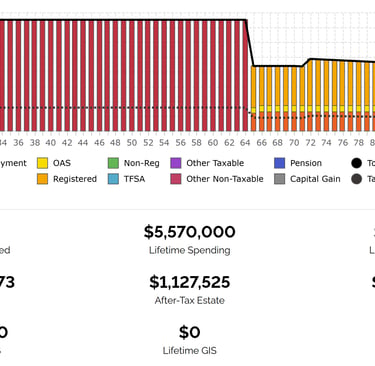

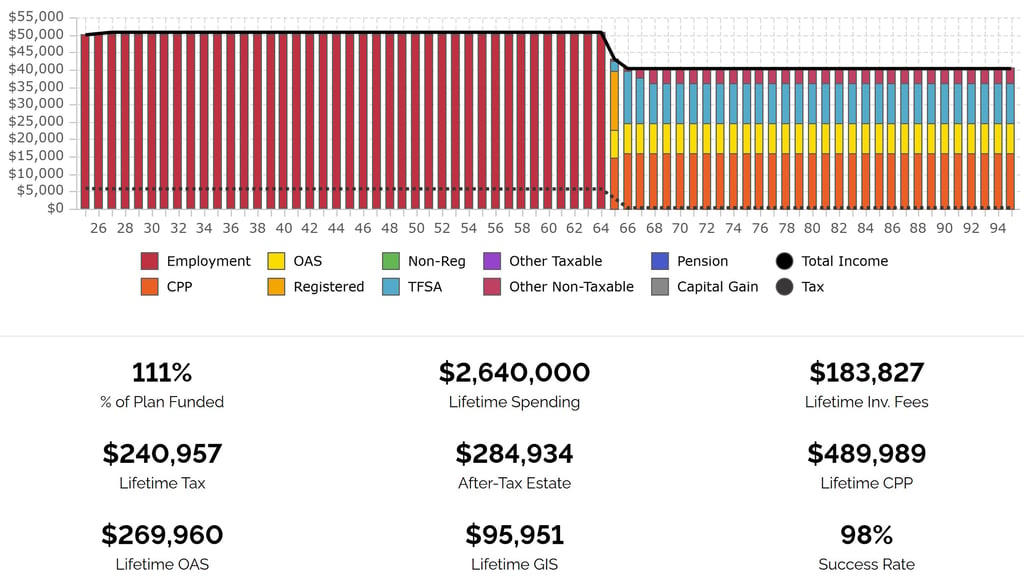

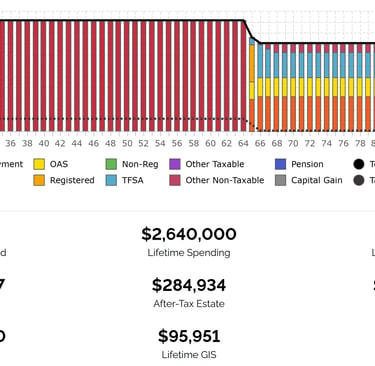

While the TFSA option might not look as exciting during the accumulation phase. It's important to remember that Clayton can't access anything in his RRSP without incurring income tax. He doesn't need to be worried about OAS claw-backs, but he would forgo the tax-free Guaranteed Income Supplement (GIS) that is available for lower income retirees in Canada. Combined with his CPP & OAS, Clayton could access nearly $28,000 per year of stable indexed income through government benefit programs as long as he lives. This causes his success rate to jump from 78% in the RRSP first scenario to 98% in the TFSA first scenario. That's a game-changer.

Clayton Annual Income Sources for TFSA Scenario

Conclusion

The TFSA is an incredibly powerful financial planning tool and using it effectively can significantly benefit almost anyone in Canada regardless of their income level. Unfortunately, many Canadians haven't been given the proper education about this account and are not considering how it can be incorporated into their financial plan. If you'd like to learn more about how you can maximize your TFSA, give us a call or Book an Intro Call.

Oakbridge Financial Planning

Strategy for the Modern Couple.

Contact Us

Legal

Email:

Phone:

© 2025. All rights reserved.

Address:

#160 - 1209 59 Ave SE Calgary, AB

T2H 2L7