When is the “Right” Time to Take CPP?

Knowing when to take CPP is an important decision as part of your retirement planning.

RETIREMENT PLANNINGFINANCIAL PLANNING

Steven

7/7/20254 min read

One question that comes up frequently in retirement planning is:

When is the right time to start Canada Pension Plan (CPP) benefits?

Almost everyone who retires in Canada will receive some form of CPP benefit during their retirement. But there is still lots of confusion about when is the right time to start taking CPP and I would argue that the analysis most frequently used can be quite misleading.

To visualize this, let’s consider an example:

John is currently 57 and planning to retire at age 60. He’s trying to decide if he should start CPP early or delay receiving the benefit for 5 or 10 years.

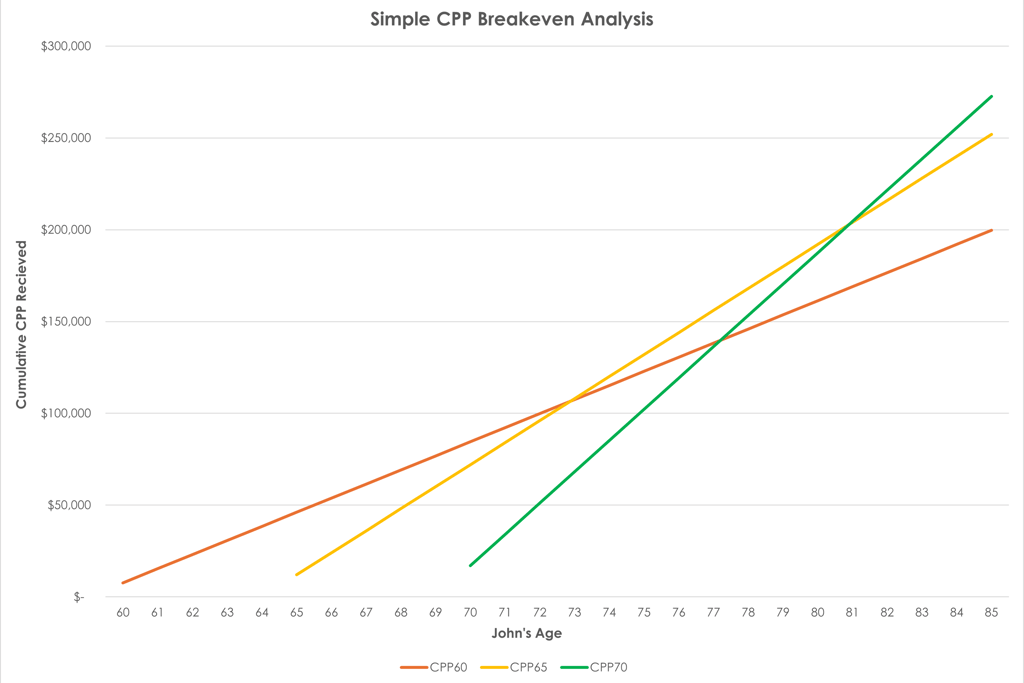

John’s scenario with simple CPP break-even analysis.

A simple CPP break-even analysis compares how much income you would receive depending on whether you start CPP at age 60, 65, or delay it to 70. The “break-even point” is the age at which the cumulative income (total amount received) from a later start (e.g., at 65 or 70) begins to exceed the amount from the earlier start.

Let’s assume John’s CPP entitlement at age 65 is $1,000/month.

Reduction if taken at 60: 36% less → $640/month

(0.6% reduction per month × 60 months)Increase if taken at 70: 42% more → $1,420/month

(0.7% increase per month × 60 months)

Looking at this chart, we can notice that:

If John takes CPP at age 60, we can see that the orange line for CPP65 crosses over the blue line for CPP60 at about age 73. Meaning that if John lives past this age, taking CPP at age 65 will result in him receiving more CPP benefits by 73 than if he had started at age 60.

The more steeply sloped green line for CPP70 that shows the larger amount John would receive each year from CPP if he waited until age 70 to start. At age 85, he's received almost $75,000 more than he would by starting at age 60.

This type of calculation can be helpful for comparison, but as you probably remember from the intro paragraph, I believe that this simple analysis can be quite misleading. There's a few reasons why:

It assumes you'll live to at least your late 70s or early 80s.

It doesn’t account for inflation, taxation, or investment returns.

It ignores your actual cash flow needs, health, or lifestyle choices.

Each of these factors plays an important role in your financial plan and excluding them from the analysis when making a CPP start age decision could impact your retirement goals. They're also likely to be different for everyone. Cookie cutters are for making cookies of the same size and shape. But people aren't cookies and each financial plan is unique.

Okay, so what's the alternative?

If simple CPP analysis isn't the best option because it doesn't consider the rest of your financial picture, then the logical assumption would be that the best type of CPP analysis is the one that does consider your full financial picture. By including the decision of when to start CPP as part of a complete financial plan, you'll be also analyze other factors alongside such as:

Your life expectancy and family health history

Your personal and household tax rates

Whether you're still working or semi-retired

Government benefits (OAS, GIS) and how CPP affects them

Your investment strategy and other income sources

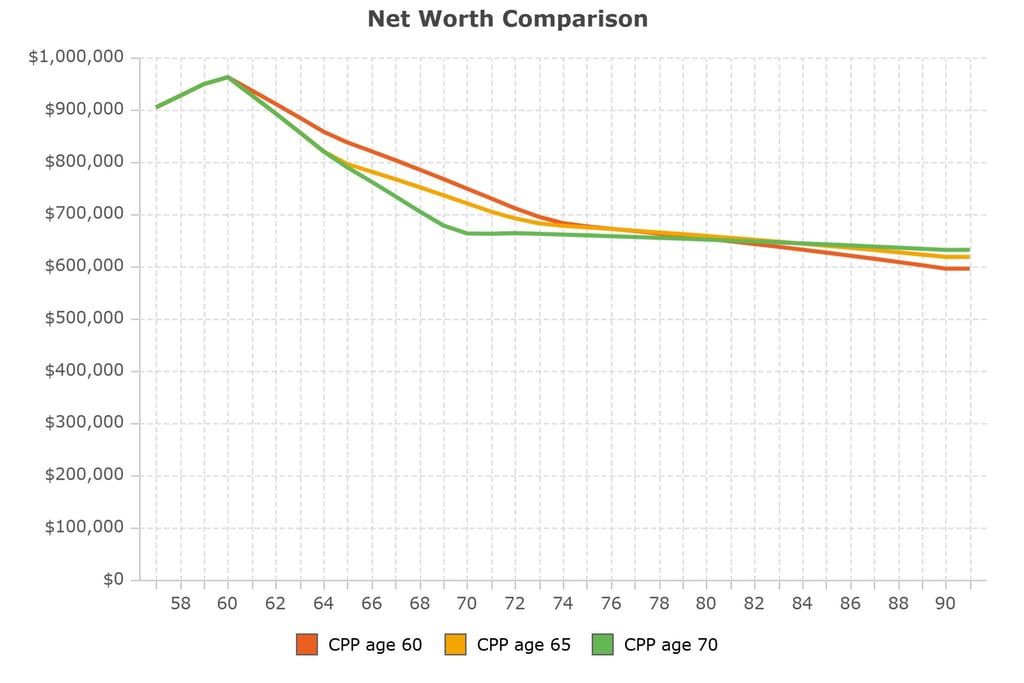

Let's work through John's retirement plan again except this time we'll use the Oakbridge financial planning tool to compare different CPP start ages for John that allows us to consider every aspect of John's financial picture as part of the analysis. Because we're not analyzing CPP in a vacuum, we're going to compare how John's net worth is impacted over his retirement.

Right away, we can see visually that this chart looks much different from the first. It's not linear and predictable because it's also factoring in John's other sources of income as well as his goals for how he'd like to spend his savings during retirement.

Compared to the points from the first graph:

The breakeven age between CPP60 and CPP65 is closer to age 76 (3 years later than with the simple analysis)

At age 85, he's still better of by choosing to start CPP at age 70, but the difference is about $16,000 (versus $75,000 when compared to the simple analysis)

If John is projected to live a long healthy retirement, both analysis methods support the recommendation that John should defer taking CPP. However, the contrast between the three alternatives is not as stark as expected when they are compared in the context of John's complete financial plan. John's unique goals and situation may lead him to choose to select an earlier CPP start age now that he can understand how this decision fits in with his retirement plan.

To conclude, the best time to start your CPP depends on more than just the simple math. It’s about what fits your overall retirement plan and gives you the most confidence and peace of mind.

If you'd like build your own financial plan and find your optimal CPP start age for only $9, CLICK HERE.

Oakbridge Financial Planning

Strategy for the Modern Couple.

Contact Us

Legal

Email:

Phone:

© 2025. All rights reserved.

Address:

#160 - 1209 59 Ave SE Calgary, AB

T2H 2L7