Is an RRSP Meltdown a Good Idea? (With Case Studies)

Knowing when and how to use an RRSP meltdown could significantly improve your retirement plan.

RETIREMENT PLANNINGFINANCIAL PLANNINGTAX PLANNING

Steven

9/4/20254 min read

RRSPs are often one of the largest assets that Canadians bring into retirement. Usually, a well-funded RRSP is the result of decades of patient and disciplined investing. However, as the focus shifts from "building" to "enjoying" your savings, it's important to reassess what the appropriate strategy is for your RRSP based on your changing goals and objectives.

The traditional approach is to defer withdrawals as long as possible and then take only the minimum from your Registered Retirement Income Fund (RRIF). This leverages the core benefit of tax deferral—your investments grow without current tax, and you pay tax only when you withdraw. A separate (but not guaranteed) benefit is tax-rate arbitrage: if you contributed in high-income years and later withdraw in lower-income years, your lifetime tax bill may be reduced.

In some cases, the traditional approach of waiting long and taking only the minimum from your RRSP/RRIFs is actually the right choice. However, it's also the strategy that requires little to no proactive planning which could mean that many retirees are actually sacrificing stability in their financial plan or even paying more in taxes without ever knowing there was an alternative option.

Two of the common issues that could impact Canadians with RRSPs during retirement are:

Reduction/loss of government benefits - Many government benefits for seniors such as Old Age Security (OAS) or Guaranteed Income Supplement (GIS) are "income-tested" meaning that large withdrawals from your RRSP/RRIF could reduce the benefits you qualify for.

Forced withdrawals above what's needed - In the year you turn 71, you are required to convert your RRSP to a RRIF and withdraw at least 5.28% (as of 2025) the following year. If you have income from other sources and don't need the funds from your RRIF, you'll still be required to make the withdrawal and pay the taxes.

What is an RRSP meltdown and when should you use it?

An RRSP meltdown is simply making one or multiple strategic withdrawals from your RRSPs before they are converted to RRIFs or above the annual minimum once they are converted. The timing and amount of these withdrawals can vary based on what's needed for each financial plan, but the end goal is to reduce the size of the retiree's RRSPs/RRIFs for financial gain or to accomplish a specific objective.

The decision of whether an RRSP meltdown strategy is right for you should always be evaluated in the context of your complete financial plan. Simply knowing the balance of your RRSP won't provide a clear answer. As mentioned earlier, a meltdown can be executed in multiple different ways and with varying degrees of intensity. The two issues listed earlier are all common financial planning challenges that can be mitigated by an RRSP meltdown. In the examples below, we'll go through a real-life instance where using a meltdown strategy enhanced the retiree's holistic financial plan.

Planning Challenge #1: Reduction/loss of government benefits

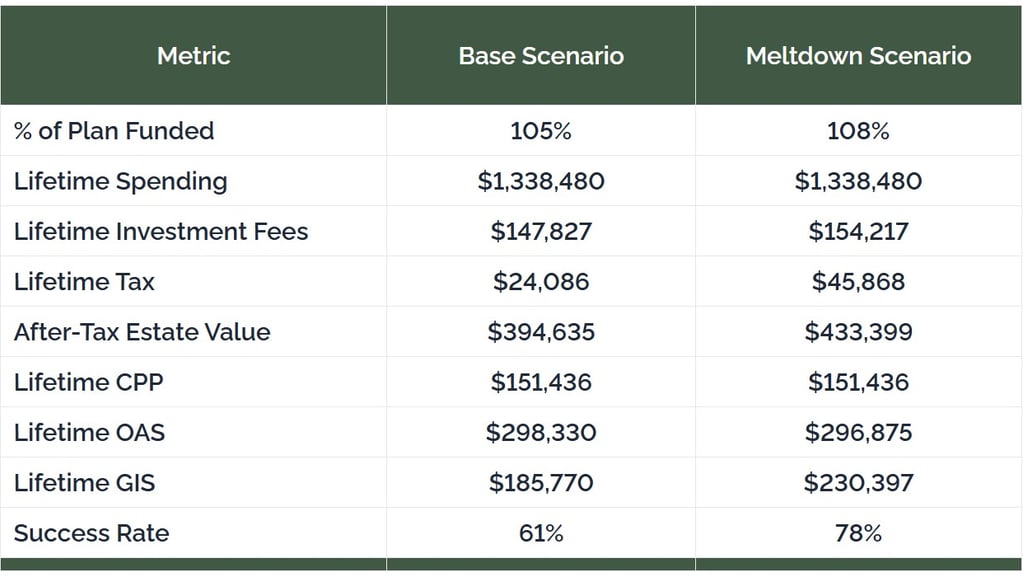

Description: Jamison, 63, would like to retire at 67. He's accumulated modest savings of $350,000 largely from an inheritance but is receiving reduced Canada Pension Plan (CPP) due to taking it early and having low career earnings. Jamison's family has a history of living into their late 90s.

Analysis: Jamison's longevity poses a problem because he will need to draw on his savings for potentially 35+ years. By using an aggressive RRSP meltdown before retirement, he is able to maximize his eligibility for GIS during retirement. This will provide stable inflation-adjusted income for his entire life.

To view the Jamison's complete plan, click here: Jamison's Financial Plan

Planning Challenge #2: Forced withdrawals above what's needed

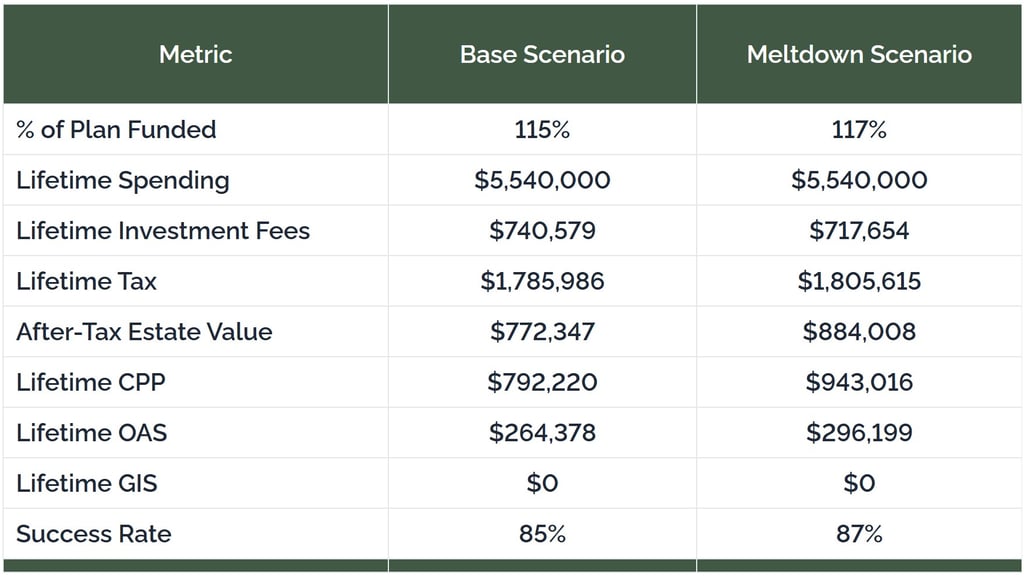

Description: Talia, 52, would like to retire at 65 or earlier if possible. She's accumulated over $1M savings in her RRSP by maxing out her contributions each year. Her retirement goals are to enjoy time with her local family as travel was a big part of her retirement. As a result, she's planning to spend less in retirement than many of her peers. She'd also like to leave an inheritance for her nieces.

Analysis: Talia has been planning from an early age and her very strong savings rate puts her in an excellent position. Using an RRSP meltdown strategy she decided to retire at 63 and defer receiving CPP and OAS until age 70. When her RRSP is converted to a RRIF at age 71, she won't be required to withdraw more than she needs to from the account and can continue to benefit from tax deferral.

To view Talia's complete plan, click here: Talia's Financial Plan

Summary

In the end, your RRSP represents decades of intentional investing. But the strategy for your retirement savings should be regularly reviewed and updated as your goals change. By aligning withdrawals with your tax brackets and benefits, you could reduce lifetime taxes, avoid clawbacks, and keep more control over your cash flow and estate. The right drawdown plan is personal—model it, choose it, and review it each year.

Oakbridge Financial Planning

Strategy for the Modern Couple.

Contact Us

Legal

Email:

Phone:

© 2025. All rights reserved.

Address:

#160 - 1209 59 Ave SE Calgary, AB

T2H 2L7